For nearly a decade, Hong Kong has quietly held the top spot in Asia’s international bond market. In 2024 alone, issuers funneled more than US$130 billion through the city. In this article we look at the factors that have given Hong Kong it's edge, primarily its unusual mix of deep liquidity, multiple currencies under one roof, a legal system ranked among the world’s most credible—and one “gateway” role that has only grown more valuable as the world fragments. From record-breaking issuances to a surprising surge few saw coming, the numbers tell a story of momentum.

This article is part of a series on London Insights. Other articles in this series deal with Hong Kong Cements Its Status as a Premier Financial Hub and Hong Kong's Enduring Appeal as an Equity Capital Markets Hub.

If you would like to make any enquiries to our London office, please contact Gavin Cumming Head of London.

"Leading Practice"

"Exceptionally Talented"

"The Choice for Sophisticated Clients"

"Leading Lawyer"

"Leading Practice"

"Global Leader"

Hong Kong's Enduring Appeal as an Equity Capital Markets Hub

Hong Kong has topped the world’s IPO rankings with US$37.4 billion raised across 119 listings. Discover how the city's equity capital markets are drawing issuers and institutional investors alike, drawn to the self-reinforcing ecosystem of liquidity, cross-border access and regulatory reform.

Hong Kong Cements Its Status As A Premier Financial Hub

For more than 150 years, Hong Kong has served as the world's gateway to China. What began as the trade of physical goods has evolved into a sophisticated two-way flow of capital, intellectual property and talent, yet throughout this period the city’s role as an indispensable intermediary remained...

Insurance Linked Securities: Hong Kong’s Insurance (Amendment) Ordinance 2020

The Insurance Amendment Ordinance 2020 enables Hong Kong insurers to issue insurance linked securities through special purpose business captives

Relaxation Of Listing Requirements On The Stock Exchange Of Hong Kong: Exit Opportunities For Private Equity?

The Stock Exchange of Hong Kong recently announced that companies whose financial situation has been temporarily and adversely affected by the current economic

SPOTLIGHT ON

FAMILY OFFICES

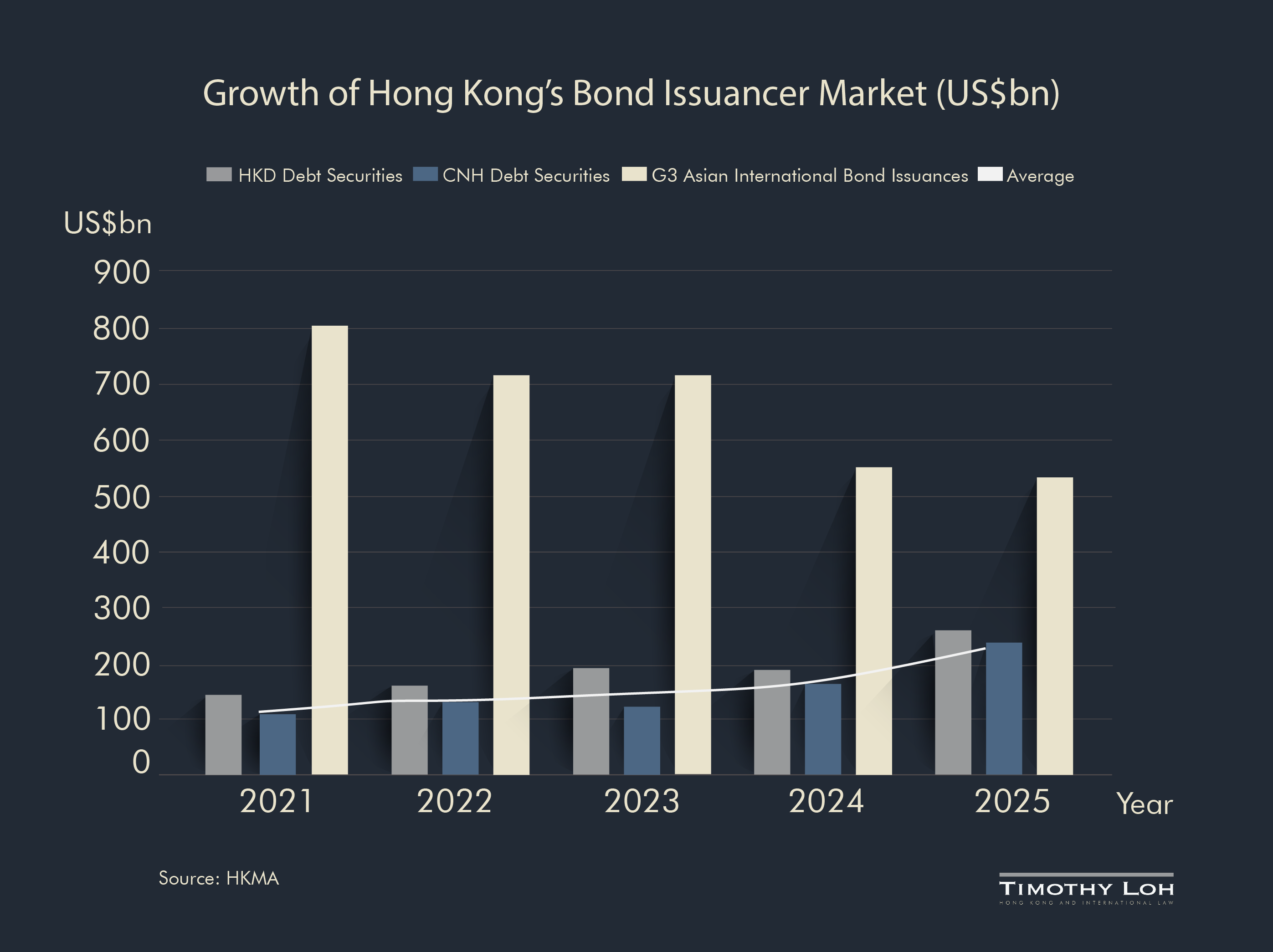

For nearly a decade, Hong Kong has occupied the top position in Asia's international bond market. In 2024 alone, issuers chose Hong Kong to arrange more than US$130 billion of international bonds, capturing approximately 30% of the regional market.

That dominance is set to spillover from the region into the world at large. What distinguishes Hong Kong from other Asian hubs is its ability to support issuance across multiple currencies within a single, internationally recognised legal and regulatory framework. Transactions span bilateral and syndicated loans, bond and debenture issuances, and other financing structures. Issuers can access Hong Kong dollars, U.S. dollars, euros, and offshore renminbi through the city's dim sum bond market.

The Foundation

At the heart of Hong Kong's appeal to debt issuers and investors are deep liquidity pools, sophisticated financial market infrastructure and global connectivity combined with a legal system that international capital markets practitioners regard as among the most credible in the world. Hong Kong's common law framework, inherited from English law and preserved under the Basic Law, provides the contractual certainty that sophisticated bond documentation demands.

“Through recent insolvency cases involving Chinese based bond issuers, we are seeing strong interest in Hong Kong law and the selection of Hong Kong itself as a venue for the resolution of disputes within the more sophisticated client base,” said Timothy Loh, Managing Partner.

That credibility is tested and demonstrated in practice. Among its most significant features for debt markets is the courts' approach to offshore bonds issued by mainland Chinese companies. Chinese corporates have long used keepwell deed structures to provide quasi-credit support for subsidiaries issuing offshore bonds, given historical repatriation constraints on overseas proceeds, and Hong Kong's courts have developed a body of jurisprudence that gives market participants a degree of certainty when those structures are tested.

A Market Built by Policy

Developing world-class bond and currency trading markets is an explicit government objective, and the authorities have backed that ambition with sustained policy action. Tax concessions for eligible issuers and investors cover a wide range of debt instruments, and targeted programmes have been introduced to stimulate specific segments of the market. A green bond financing scheme launched in 2021 positioned Hong Kong as Asia's leading sustainable finance hub, and the results are visible in the data: the city now captures around 70% of debt issuances across the region and approximately 45% of green and sustainable bond transactions.

Offshore renminbi bond issuance hit RMB1.07 trillion (US$160 billion) in 2024, a 37% year-on-year increase. More surprising has been a jump in Hong Kong dollar denominated bond issuance. Global and local entities raised a record US$9.4 billion in local currency issuances in the first four months of 2026 alone, according to Bloomberg, as tighter yields compared to U.S. dollar rates drew opportunistic issuers to the market. By comparison, annual Hong Kong dollar denominated issuances averaged around US$1.5 billion between 2018 and 2025.

The China Gateway

Perhaps no structural advantage is more distinctive than Hong Kong's role as the world's premier offshore gateway both to mainland Chinese capital markets and to mainland Chinese issuers. Under the "One Country, Two Systems" framework, Hong Kong operates as part of China yet functions under a separate regulatory and monetary regime, a combination that makes it uniquely attractive for both Chinese issuers accessing international investors and international investors seeking China exposure.

The global environment of recent years has reinforced rather than diminished this role. As US-China tensions and the broader fragmentation of global trade have made direct access to mainland markets more complex for many international investors, Hong Kong's position as a trusted intermediary has become more valuable. At the same time, as trade with China continues to grow in many countries, pressure to settle in renminbi rises and along with it, the need for reniminbi denominated fixed income instruments to hold the currency.

Bond Connect, launched in 2017 and steadily expanded since, has cemented Hong Kong’s position as an intermediary. By the end of 2025, 839 global institutional investors were accessing China's interbank bond market via Hong Kong, with annual trading turnover reaching RMB27.8 billion (US$4.1 billion)

"Hong Kong is the Asian centre for debt capital issurance for good reason,” said Gavin Cumming, Partner and Head of London at Timothy Loh. “It is the result of decades of incremental policy and judicial decisions that gives investors confidence this is the preferred hub for issuing and trading debt instruments.”