For nearly a decade, Hong Kong has quietly held the top spot in Asia’s international bond market. In 2024 alone, issuers funneled more than US$130 billion through the city. So what gives Hong Kong it's edge? The answer lies in an unusual mix of deep liquidity, multiple currencies under one roof, a legal system ranked among the world’s most credible—and one “gateway” role that has only grown more valuable as the world fragments. From record-breaking issuances to a surprising surge few saw coming, the numbers tell a story of momentum.

This article is part of a series on London Insights. Other articles in this series deal with Hong Kong Cements Its Status As A Premier Financial Hub and Hong Kong’s Debt Markets Come Into Their Own.

If you would like to make any enquiries to our London office, please contact Gavin Cumming Head of London.

"Leading Practice"

"Exceptionally Talented"

"The Choice for Sophisticated Clients"

"Leading Lawyer"

"Leading Practice"

"Global Leader"

Hong Kong’s Debt Markets Come Into Their Own

Discover why Hong Kong is dominating Asia's international bond market, from offshore renminbi bonds to green finance. Explore the legal and policies that are driving this rise.

Hong Kong Cements Its Status As A Premier Financial Hub

For more than 150 years, Hong Kong has served as the world's gateway to China. What began as the trade of physical goods has evolved into a sophisticated two-way flow of capital, intellectual property and talent, yet throughout this period the city’s role as an indispensable intermediary remained...

Insurance Linked Securities: Hong Kong’s Insurance (Amendment) Ordinance 2020

The Insurance Amendment Ordinance 2020 enables Hong Kong insurers to issue insurance linked securities through special purpose business captives

Unified Funds Tax Exemption: Relief for OFCs and Other Hedge Funds and Private Equity Funds

The Unified Funds Tax Exemption exempts OFCs, hedge & private equity funds from profits tax without offshoring central management and control

SPOTLIGHT ON

FAMILY OFFICES

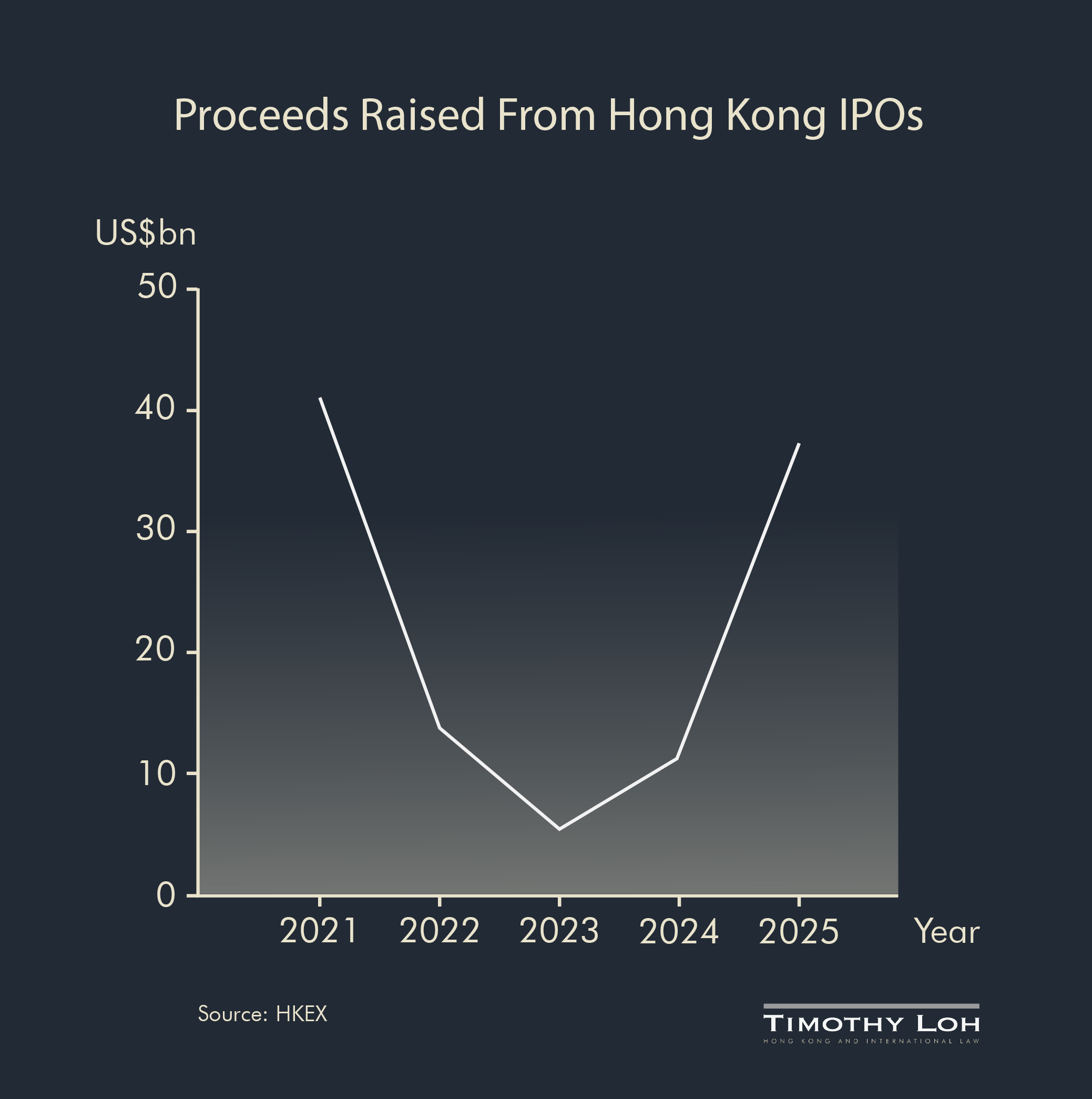

After several lean years, Hong Kong has reasserted itself as one of the world's premier venues for equity capital market activity. Total ECM fundraising surged 164% year-on-year to US$103 billion, encompassing IPOs and follow-on offerings, with IPO proceeds alone reaching US$37.4 billion across 119 listings, the highest figure since 2021.

Those numbers meant Hong Kong’s stock exchange (HKEX) topped the world rankings for IPO listings last year, with two of the five largest IPOs globally debuting on the bourse.

Hong Kong's foundational appeal is its role as the only international financial centre under a common law legal system that offers deep, two-way access to one of the world's largest economies. That connectivity has fuelled the growth of an ECM ecosystem that’s attracted institutional investors and intermediaries helping further establish Hong Kong as one of the world’s premier financial centres.

Stock Connect Provides Infrastructure Advantage

A key innovation has been the Stock Connect programme, which has linked the city’s bourse with the Shanghai and Shenzhen exchanges since 2014, and enables investors on both sides of the border to trade each other’s market. The project has expanded progressively to cover bonds, ETFs, and interest rate swaps.

As of early 2026, Southbound trading covered 564 Hong Kong-listed stocks and 23 ETFs, while Northbound encompassed over 3,200 A-shares and 365 ETFs. The A+H dual-listing structure, under which companies list simultaneously on a mainland exchange and in Hong Kong, has become a particularly powerful fundraising vehicle: in the first half of 2025 alone, eight A+H listings contributed US$10.1 billion of IPO proceeds.

That cross-border liquidity pool has also proven a draw for international issuers with companies from the U.S., Southeast Asia and the Middle East raising more than US$5 billion last year.

"Our firm is seeing institutional and corporate investors leveraging Hong Kong for regulated and liquid access to Chinese assets. Similarly, mainland Chinese investors are leveraging Hong Kong to access a international institutional and corporate investor base - a combination no other place offers. This results in clear, distinct advantages for Hong Kong as an ECM centre,” said Timothy Loh, Managing Partner.

Tax, Regulation and the Institutional Investor Draw

Tax efficiency is a further draw. The city’s low-tax environment accommodates efficient structures for issuers and fund managers alike, alongside an internationally recognised regulatory environment. Together, these features attract the institutional investors whose participation creates the deep liquidity pools that in turn draw issuers to the market, a self-reinforcing dynamic that has taken decades to build.

Sustained regulatory reform has progressively widened the market's appeal beyond its traditional base of large-cap Chinese listings. In 2023, HKEX created Chapter 18C, a dedicated pathway for early stage specialist technology companies. Last May last year, HKEX launched the Technology Enterprises Channel, providing pre-listing guidance for specialist technology companies and biotech firms. The results are already visible: Hong Kong hosted 14 pre-revenue biotech listings in 2025, up from just 4 in 2024.

Chinese and Hong Kong regulators have also streamlined cross-border listing approval processes shortening the path for mainland issuers. HKEX is currently deliberating changes to weighted voting rights rules in order to enhance the route for overseas listed issuers to come to Hong Kong, among other structural improvements.

"Hong Kong's appeal as an ECM centre rests on durable structural advantages,” said Gavin Cumming, Partner and Head of London at Timothy Loh. “Its unique position as the gateway between China and international capital, a robust common law framework, progressive listing reforms, and Stock Connect infrastructure that no rival can replicate quickly,”