Under s. 45 of the Stamp Duty Ordinance, transfers of Hong Kong stock and immovable property are exempt from Hong Kong stamp duty where the transferor and transferee are associated bodies corporate. Though the definition of an associated body corporate relies upon the concept of “issued share capital”, a recent court decision confirms that bodies corporate without equity interests referred to in common parlance as “shares”, such as English limited liability partnerships(“LLPs”) and U.S. limited liability companies (“LLCs”), may nevertheless qualify for relief. Should you wish to find out more about exemptions from Hong Kong stamp duty, please contact one of our tax lawyers.

[Updated August 3, 2025 - See commentary on Court of Appeal decision reversing this District Court decision and the Court of Final Appeal decision affirming the Court of Appeal's reversal].

"Leading Practice"

"Exceptionally Talented"

"The Choice for Sophisticated Clients"

"Leading Lawyer"

"Leading Practice"

"Global Leader"

Hong Kong Tax Concessions Succeed in Drawing Family Offices

Learn how the newly introduced tax concessions have created more family offices in Hong Kong and how family office transactions could be eligible for a zero tax

Dealing with Profits Tax Challenges: FAQs on IRD Audits & Investigations

IRD audits and investigations for profits tax on Hong Kong businesses. This article delves into the processes that trigger inquiries, addressing common question

Hong Kong Income Tax - Agency Arrangements in a Territorial Tax System

Hong Kong court rejects taxpayer’s offshore income claim, ruling taxpayer’s profit producing activities excluded agent’s activities outside Hong Kong.

Source of Profits – The Foreign Sourced Income Exemption Regime in Hong Kong

We discuss the refinements to HK’s FSIE regime, IRO provisions deeming foreign income to be sourced in HK and how those may be exempted from profits tax.

SPOTLIGHT ON

FAMILY OFFICES

Section 45 of the Stamp Duty Ordinance (“SDO”) provides an intra-group exemption from stamp duty for instruments transferring a beneficial interest in Hong Kong stock or immovable property between associated bodies corporate. Under the SDO, the bodies corporate are associated if:

“one is beneficial owner of not less than 90 per cent of the issued share capital of the other, or a third such body is beneficial owner of not less than 90 per cent of the issued share capital of each”.

Though the Stamp Duty Office has historically accepted that limited liability companies and limited liability partnerships which are separate legal persons may qualify for relief under s. 45, recent practice has evolved so that such bodies corporate have been refused relief on the basis that such bodies lack “issued share capital” and thus, cannot meet criteria for association.

The recent District Court decision on John Wiley & Sons UK2 LLP & Anor v The Collector of Stamp Revenue [2022] HKDC 716 restores the historical position, affirming that bodies corporate whose equity interests are not commonly unitized into “shares” can nevertheless qualify for association and thus, exemptive relief.

The Facts

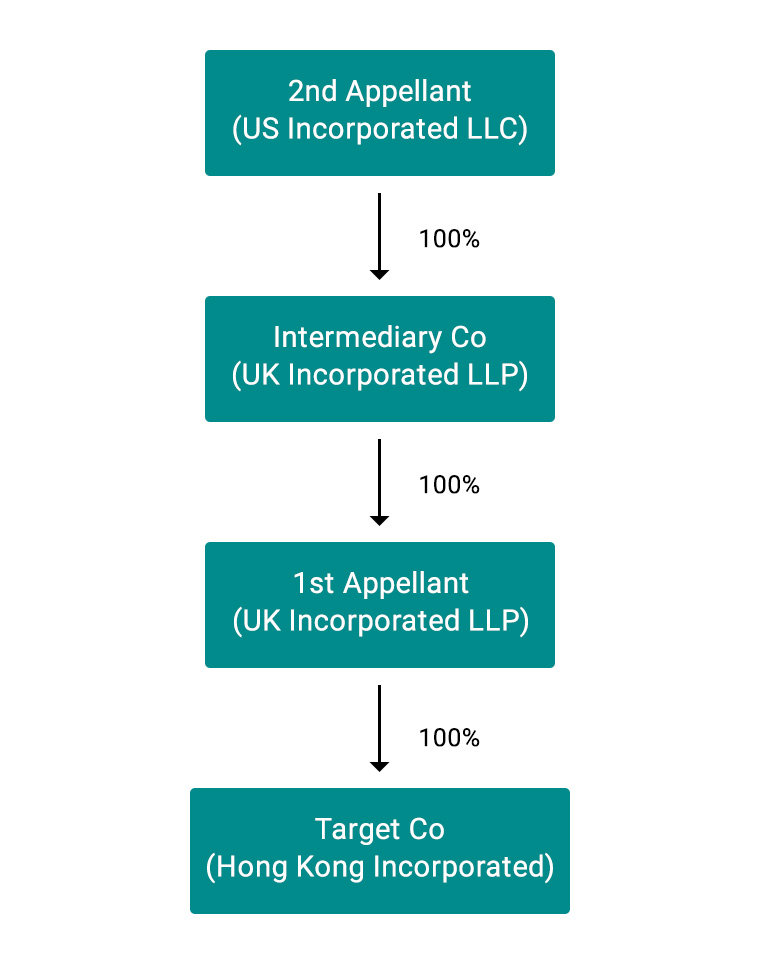

In this case, the 2 appellants were part of the same corporate group. The 1st appellant (“1st Appellant”) was indirectly wholly owned by the 2nd appellant (“2nd Appellant”) through an intermediary company (“Intermediary Co”). The 1st Appellant and the Intermediary Co were both LLPs incorporated in the United Kingdom, and the 2nd appellant was a limited liability corporation incorporated in the State of Delaware of the United States. Under the laws of the United Kingdom, LLPs are separate legal persons.

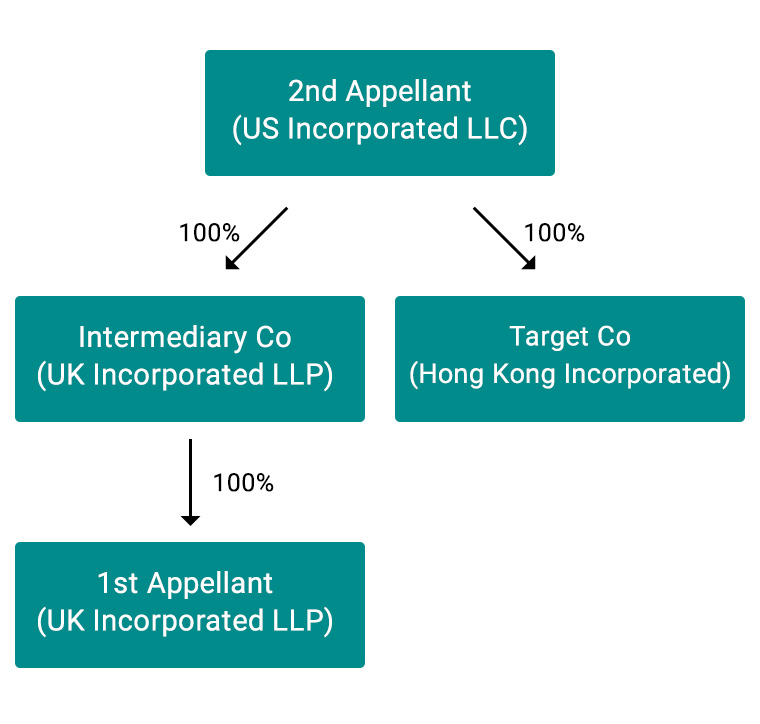

As part of an internal group restructuring, the 1st Appellant transferred its entire shareholding of a Hong Kong company (“Target Co”) to the 2nd Appellant. The end result of this share transfer was that the Target Co ceased to be a directly wholly owned subsidiary of the 1st Appellant and became a directly wholly owned subsidiary of the 2nd Appellant.

The organizational chart below shows the structure of the group before the share transfer:

The organizational chart below shows the structure of the group after the share transfer:

Following the completion of the share transfer, the appellants applied for the stamp duty relief under s. 45 of the SDO. The appellants’ application was rejected by the Collector of Stamp Revenue (“Collector”). The Collector was of the view that though the 1st Appellant and the Intermediary Co at material times were bodies corporate, they lacked “issued share capital” and therefore, could not be associated for the purpose of s. 45 of the SDO. The appellants subsequently lodged an appeal against the assessment to the District Court.

The Law

The Court rejected the Collector’s arguments and allowed the appeal.

The Court accepted that the term “issued share capital” was not defined by the SDO. Applying the well-established purposive approach of statutory interpretation, the Court observed that the legislative purpose of s. 45 was to grant stamp duty relief in circumstances where 2 companies involved in the transfer were associated with each other so closely that the transfer was little more than a change in the nominal ownership, rather than a change in the ultimate beneficial ownership.

Bodies Corporate

The Court then looked at the legislative history of s. 45. The section was originally s. 5A of the old SDO. When the Legislature amended s. 5A, it replaced the term “companies with limited liability” with the term “bodies corporate”. The Court took the view that such amendment showed the legislature’s intention to open up the ambit of s. 45 relief to encompass all associated groups, regardless of whether their relevant members were incorporated as companies with limited liability or incorporated in other forms of bodies corporate in or outside Hong Kong.

Issued

In light of the legislative purpose and history of s. 45, the Court held that the word “issued” should be interpreted to mean “having been legally given to (those entitled to the share capital) in a legally completed transaction”.

Share Capital

The Court went on to hold that the term “share capital” should not be interpreted to mean that the capital of a body corporate must be divided by way of a denomination into standard units called “shares” that are required to be registered or evidenced by share certificates. Instead, a body corporate would have “share capital” as long as the capital of the body corporate was divided (such division should be legally recognized by the laws of the jurisdiction where the body corporate was incorporated) into quantifiable portions, whether expressed in terms of monetary value or in term of proportions, and all such portions together make up 100% of the total value of the capital.

Court Decision

Applying the interpretation above, since the capital of each of the 1st Appellant and the Intermediary had a nominal value and had been divided into 2 portions expressed in monetary value, which had been taken up and paid for by the initial members, the Court held that the 1st Appellant and the Intermediary had “issued share capital” and therefore could be regarded as associated bodies within the meaning of s. 45.